I’m a firm believer that information is the key to financial freedom. On the Stilt Blog, I write about the complex topics — like finance, immigration, and technology — to help immigrants make the most of their lives in the U.S. Our content and brand have been featured in Forbes, TechCrunch, VentureBeat, and more.

See all posts Frank GogolAnalysis: Student Debt Grew 148% Between 2013 and 2023 as Default Surged 240% to $104 Billion

Updated on February 21, 2024

Written by

Written by

Key Takeaways:

- Student loan debt in the U.S. has surged 148% to $1.4 trillion in 2023.

- Over 10% of student borrowers are currently in default.

- Student loan defaults have increased by 240% since 2013.

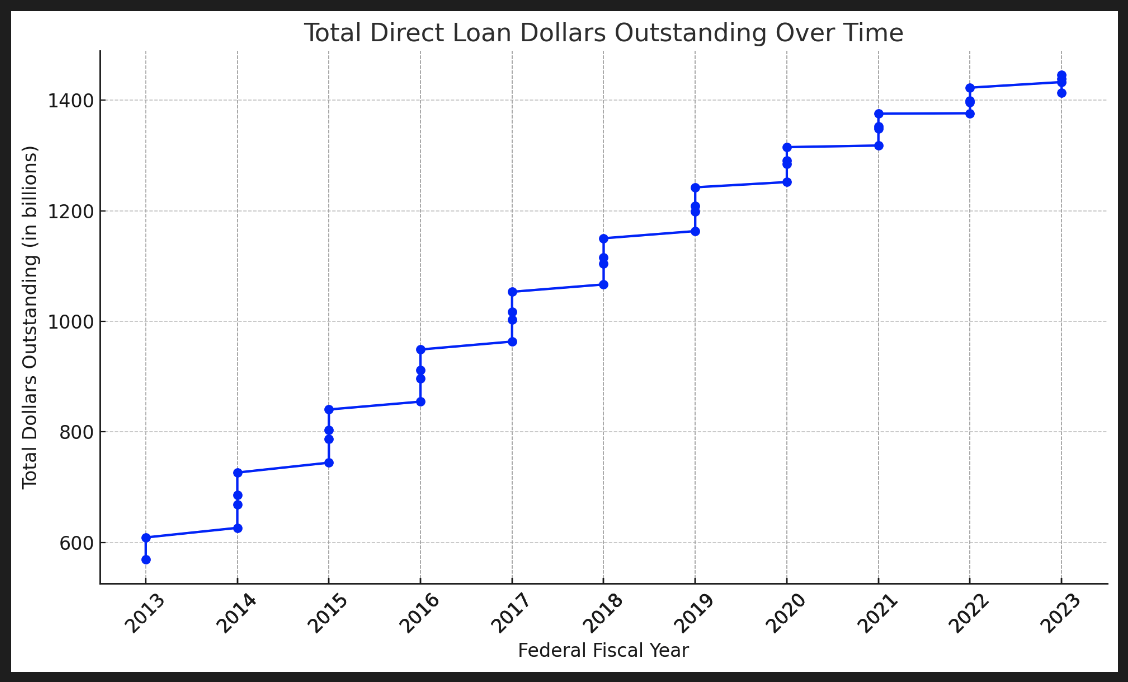

In the last decade, the United States has witnessed an unprecedented surge in student loan debt, transforming it from a widespread concern into an acute crisis that now looms over millions of Americans. This burgeoning debt epidemic not only shackles the financial futures of a generation but also casts long shadows over their career choices and life aspirations. With an alarming 148% increase in the total direct loan dollars outstanding, from $569.2 billion to a staggering $1.4 trillion, the crisis encapsulates the daunting challenges and systemic issues plaguing higher education financing. As we delve deeper into the ramifications of this crisis – via the National Student Loan Data System’s (NSLDS) Direct Loan Portfolio by Loan Status dataset – it becomes evident that the implications extend far beyond mere numbers, affecting the very fabric of American society.

Student Loan Debt Surged 148% Over Last Decade

The issue of student loan debt in the United States has dramatically shifted from a mere concern to a full-blown crisis over recent years, profoundly affecting millions of Americans. The financial strain imposed by the rising costs of higher education is far from a mere statistic; it is a palpable reality that influences the financial health, career paths, and pivotal life decisions of an entire generation. A detailed analysis of the Direct Loan Portfolio by Loan Status highlights this troubling trend with a staggering 148% increase in total direct loan dollars outstanding, escalating from $569.2 billion to $1.4 trillion. This sharp uptick not only underscores a deepening crisis but also reflects the growing cumulative debt—principal plus interest—shouldered by students year after year.

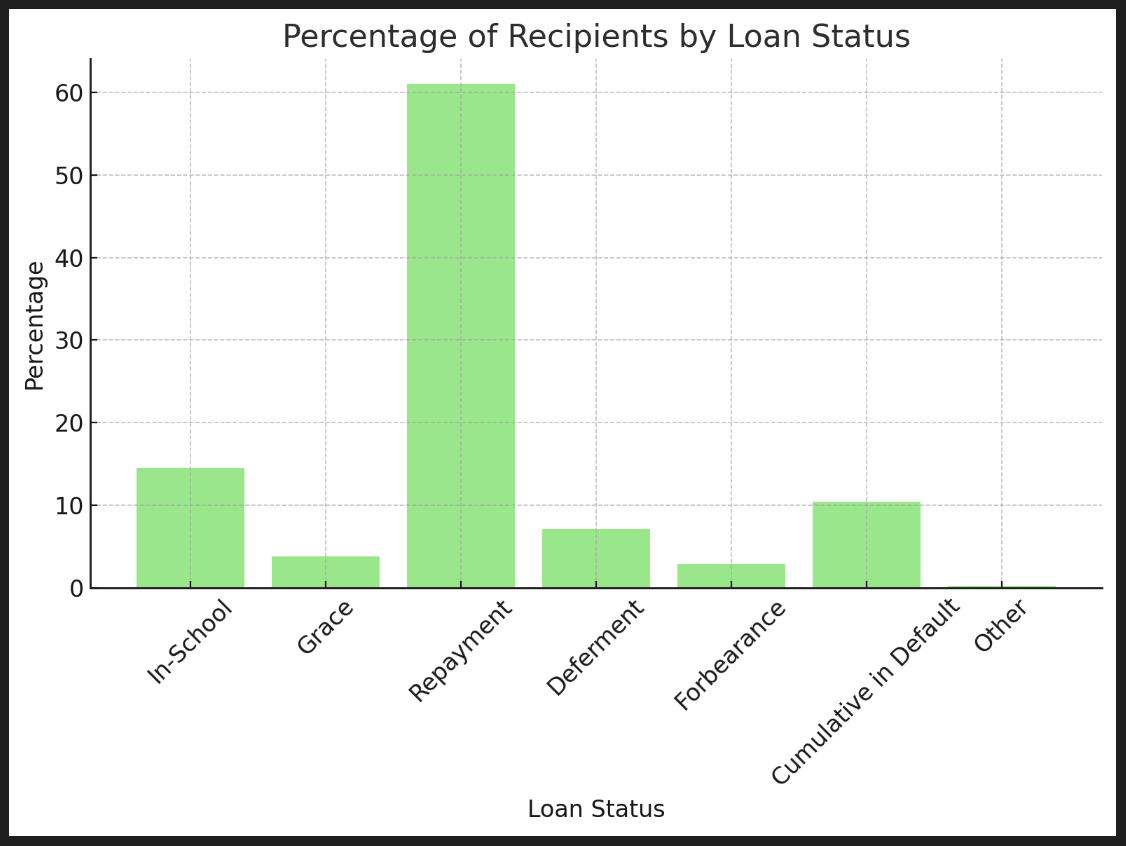

Over 10% of Student Borrowers are in Default Today

Recent federal data on student

A closer examination of the federal data sheds light on a crisis at a critical juncture in the repayment lifecycle. While current students and those in their grace period represent 10% of the total debt, the bulk—70%—are borrowers actively attempting to repay their

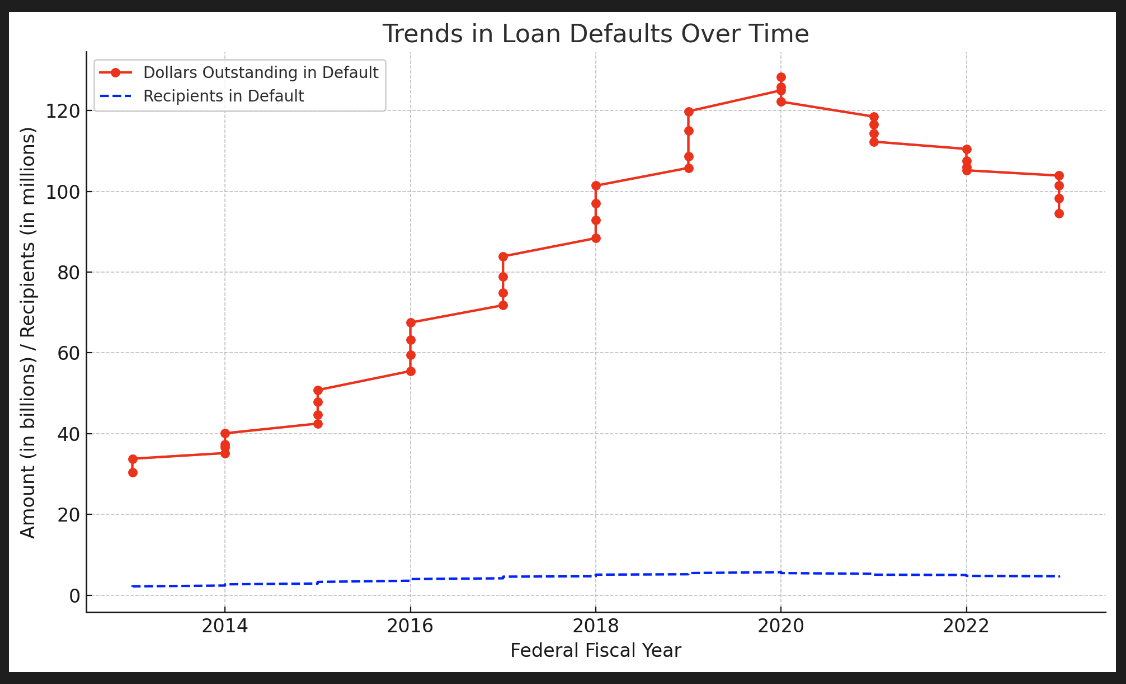

Student Loan Defaults Surged 240% to $104 Billion

The past decade, spanning from 2013 to 2023, has seen the student loan landscape in the U.S. plunge deeper into a default crisis, marking a period of escalating financial distress for borrowers nationwide. An in-depth look into federal data exposes alarming trends in both the volume of debt falling into default and the expanding number of borrowers affected.

Notably, the amount of debt categorized as in default has surged by an astonishing 240%, climbing from $30.5 billion to $103.9 billion over the ten-year timeframe. This dramatic increase not only mirrors the escalating financial burden borne by borrowers but also highlights the intensifying challenges surrounding loan repayments. Equally troubling is the 123% surge in the number of borrowers finding themselves in default, more than doubling from 2.1 million to 4.7 million individuals. This significant rise further accentuates the growing predicament facing borrowers and underscores the urgency for systemic reforms within the student loan system.

Final Thoughts

As we confront the stark realities presented by the surging student loan debt and the alarming rate of defaults in the United States, it becomes clear that this crisis transcends individual financial struggles, embedding itself deeply within the societal and economic fabric of the nation. The data not only highlights the urgent need for comprehensive policy reforms and support systems but also calls for a collective reevaluation of the value and accessibility of higher education. Addressing this crisis requires a multifaceted approach, aimed at alleviating the immediate financial burdens on borrowers while fundamentally reimagining the structure of education financing. Only through concerted efforts can we hope to mitigate the impacts of this crisis and pave the way for a future where higher education serves as a bridge to opportunity, rather than a barrier burdened by debt.

About This Data

In our exploration of the student loan landscape, we’ve delved into the intricacies of the Direct Loan Portfolio by Loan Status, a comprehensive dataset that offers a window into the financial burdens borne by millions of student loan borrowers in the United States. This data, drawn from the National Student Loan Data System, provides a detailed breakdown of outstanding principal and interest balances across various loan statuses, offering insights into trends over time and the distribution of debt among borrowers.

The Scope of the Dataset

The dataset encompasses a wide range of loan statuses, each reflecting a different phase in the borrower’s journey:

- In-School: Loans for students currently enrolled in higher education, highlighting the inception of the debt journey.

- Grace:

Loans in their grace period post-graduation, before repayment begins, indicating a transition phase for recent graduates. - Repayment:

Loans actively being repaid by borrowers, representing the primary phase of the debt cycle. - Deferment:

Loans temporarily paused due to specific conditions such as unemployment or further education, offering temporary relief to borrowers. - Forbearance:

Loans on which payments are temporarily reduced or suspended due to financial hardship, indicating borrowers in distress. - Cumulative in Default: Loans that have failed to be repaid according to the terms of the agreement, reflecting severe financial challenges.

- Other: A category encompassing

loans that do not fit neatly into the other statuses, providing a catch-all for anomalies and special cases.

Methodology

The methodologies adopted for the analyses in this article were designed to illuminate the trends, distributions, and impacts of student loan debt, providing a comprehensive picture of the challenges and burdens faced by borrowers. Here, we detail the methodologies used to derive the insights shared in our analysis.

Trends Over Time Analysis

- Objective: To understand how the total direct loan dollars outstanding has evolved over the available federal fiscal years.

- Data Aggregation: We summed the dollars outstanding across all loan statuses for each federal fiscal year to calculate the total outstanding student loan debt per year.

- Trend Visualization: The total dollars outstanding for each year were then plotted over time, creating a line graph that visually represents the trend of increasing student loan debt.

Loan Status Distribution Analysis

- Objective: To examine the distribution of loan statuses, identifying where the majority of the debt and borrowers are concentrated.

- Percentage Calculation: For each loan status, we calculated the percentage of the total dollars outstanding and the percentage of total recipients. This approach allowed us to understand not just where the debt is concentrated but also where most borrowers are situated in their loan lifecycle.

- Comparative Visualization: The percentages were visualized using bar charts, one for the distribution of dollars outstanding and another for the distribution of recipients, providing a clear comparative analysis of the loan status distribution.

Default Rates and Impacts Analysis

- Objective: To assess the scale and growth of defaulted

loans , focusing on the “Cumulative in Default” category over time. - Trend Analysis: We plotted the dollars outstanding in default and the number of recipients in default over the available federal fiscal years to visualize the trends.

- Change Quantification: By comparing the initial and final values for both metrics, we quantified the increase in defaults, both in terms of dollars and the number of affected borrowers, providing a clear picture of the growing default crisis.

Ensuring Accuracy and Relevance

In all analyses, care was taken to ensure data accuracy and relevance. The dataset was meticulously cleaned and preprocessed to address any inconsistencies or missing values. Furthermore, we focused on the most recent data available to ensure that our insights reflect the current state of the student loan landscape.

The methodologies employed in these analyses are rooted in a commitment to providing a data-driven understanding of student loan debt. By dissecting the data through these lenses, we aim to contribute meaningful insights that can inform policy discussions, support advocacy efforts, and ultimately help borrowers navigate the complexities of student loan debt.

Considerations and Limitations

While the analysis of the Direct Loan Portfolio by Loan Status offers valuable insights into the student loan landscape, it’s important to acknowledge the inherent considerations and limitations of this data. Understanding these nuances is crucial for accurately interpreting the findings and for informing the development of policies and strategies aimed at addressing the challenges of student loan debt.

- Data Scope and Coverage: The dataset primarily focuses on direct

loans , which, while encompassing a significant portion of student loan debt, does not include all types of student financing, such as privateloans orloans from the Federal Family Education Loan (FFEL) Program. This limitation means that our analysis might not fully capture the entirety of the student loan burden faced by individuals. - Temporal Constraints: Our analysis is bounded by the federal fiscal years for which data is available. Changes in policies, economic conditions, and borrowing behaviors that occur outside of these time frames may influence the student loan landscape in ways not reflected in our analysis. Additionally, the most recent year’s data may not fully account for ongoing developments or the impact of recent policy changes.

- Lack of Demographic and Socioeconomic Data: The dataset does not provide detailed demographic or socioeconomic information about borrowers, limiting our ability to analyze how student loan debt affects different groups within the population. Factors such as race, gender, income level, and type of institution (e.g., public vs. private, for-profit vs. nonprofit) play critical roles in the student loan experience but are not captured in this analysis.

- Economic and Policy Context: The data analysis does not directly account for broader economic conditions or specific policy changes that may impact student loan debt trends. For instance, economic recessions, changes in interest rates, and alterations in loan forgiveness or repayment programs can significantly affect borrowing and repayment behaviors.

- Interpretation of Trends: While the analysis provides a snapshot of trends and distributions within the student loan system, interpreting these trends requires caution. Correlation does not imply causation, and the factors contributing to increases in debt, defaults, or changes in loan status distribution are complex and multifaceted.

- Moving Forward: Despite these limitations, the analysis of the Direct Loan Portfolio by Loan Status offers critical insights into the dynamics of student loan debt. It highlights the urgent need for comprehensive solutions to support borrowers and mitigate the financial challenges posed by student loan debt. As we move forward, it’s essential to complement this analysis with additional research that addresses these limitations, incorporating a broader range of data sources, demographic insights, and economic indicators. Doing so will provide a more complete understanding of the student loan landscape and inform more effective policy and support interventions.

Frank Gogol

I’m a firm believer that information is the key to financial freedom. On the Stilt Blog, I write about the complex topics — like finance, immigration, and technology — to help immigrants make the most of their lives in the U.S. Our content and brand have been featured in Forbes, TechCrunch, VentureBeat, and more.