I’m a firm believer that information is the key to financial freedom. On the Stilt Blog, I write about the complex topics — like finance, immigration, and technology — to help immigrants make the most of their lives in the U.S. Our content and brand have been featured in Forbes, TechCrunch, VentureBeat, and more.

See all posts Frank GogolStilt Analysis: Over Half of U.S. Bank Failures Since 2000 Occurred Outside the Great Recession

Updated on February 5, 2024

Written by

Written by

Highlights

- Half of All Bank Failures Since 2000 Occurred Outside the Great Recession

- Nearly 200 Banks Failed in Just 3 States Since 2000

- Almost 85% of Failed Banks Were Acquired by Local Institutions

- Large Banks Grew Assets by 2-3x Through Failed Bank Acquisition

The financial crisis of 2008 tipped the economy into turmoil, sending ripple effects throughout the banking industry. As home prices collapsed and toxic assets racked up, banks failed at an astonishing rate. New analysis of FDIC data on bank failures reveals both nationwide trends as the crisis crescendoed, as well regional insights into the hardest-hit states. By investigating bank consolidation patterns, the post also uncovers clues about the size and types of banks that fell. Ultimately, the crisis dealt a crushing blow, but the system emerged more prudent than ever.

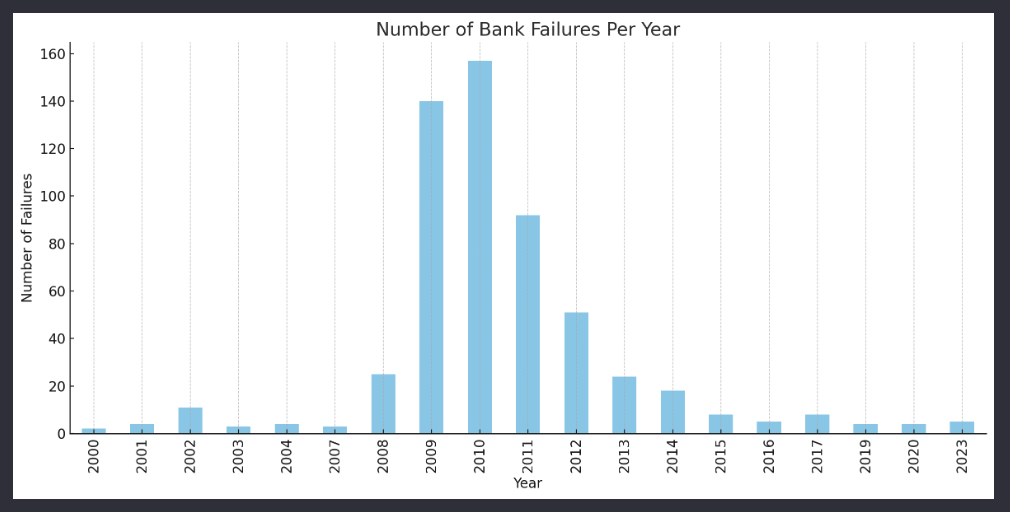

50% of Bank Failures Since 2000 Occurred Outside the Great Recession

The financial crisis that began in 2008 tipped many banks over the edge, as reflected clearly in bank failure data. The years 2009 and 2010 stand out as the most turbulent years for bank closures, according to the Federal Deposit Insurance Corporation’s (FDIC) Failed Bank List. An astounding 140 banks failed in 2009 at the height of the Great Recession, followed by 157 in 2010. This two-year period accounts for nearly one-third of all bank failures since 2000.

Prior to the crisis, bank failures held relatively steady in the single or low double digits each year. Once the recession hit, however, banks large and small succumbed to souring

Since peaking in 2010, the number of bank failures has steadily declined each year as the economy slowly recovered. By 2015, closures dropped to single digits for the first time post-crisis. From 2016 to 2023, bank failures have remained consistently low at under 10 per year despite some fluctuations.

As the economy has normalized, so have bank failure rates. However, it took several years to absorb and overcome the damage from the financial crisis. The crisis permanently reshaped the banking industry, leaving the survivors much more risk-averse and regulated. But the system-wide weaknesses that led to such a wave of closures have largely been remedied.

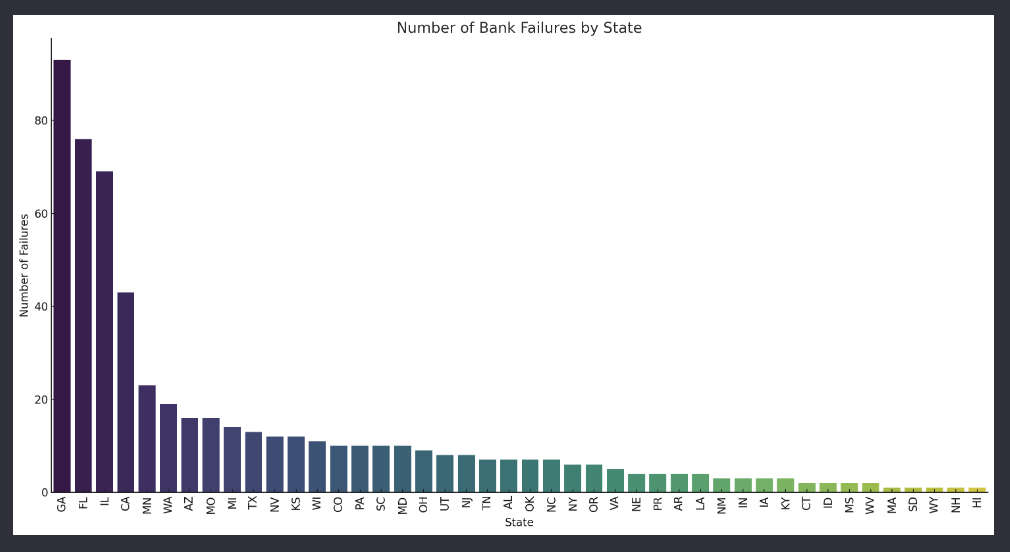

Nearly 200 Banks Failed in Just 3 States Since 2000

While the financial crisis caused bank failures nationwide, some states were impacted more than others. According to the FDIC records, Georgia suffered the highest number of bank casualties with 93 institutions closing their doors. Florida followed closely behind with 76 failures. Rounding out the top 3 is Illinois with 69 banks shutting down.

California and Minnesota also incurred major damage, experiencing 43 and 42 bank failures respectively. Other hard-hit states include Washington (40 failed banks), Arizona (33), Missouri (31), Michigan (30), and Texas (28).

Clearly, the crisis did not spread evenly across the country. There seems to be a geographical concentration of failures in the Southeast, Southwest, and parts of the Midwest. The common thread connecting the most impacted states appears to be major real estate markets that overheated and then went bust during the subprime mortgage meltdown. States like California, Florida, Arizona and Georgia saw some of the most dramatic home price increases and declines.

Additionally, the sheer size of the banking sectors in states like New York and California meant more institutions were exposed to high-risk investments and

While myriad factors contributed to each bank failure, the geographic distribution highlights regions where economic instability and weaknesses in the banking industry collided. The convergence of downturns in key industries like real estate and finance with underlying issues in regulation and risk management ultimately determined where banks toppled the fastest when crisis hit.

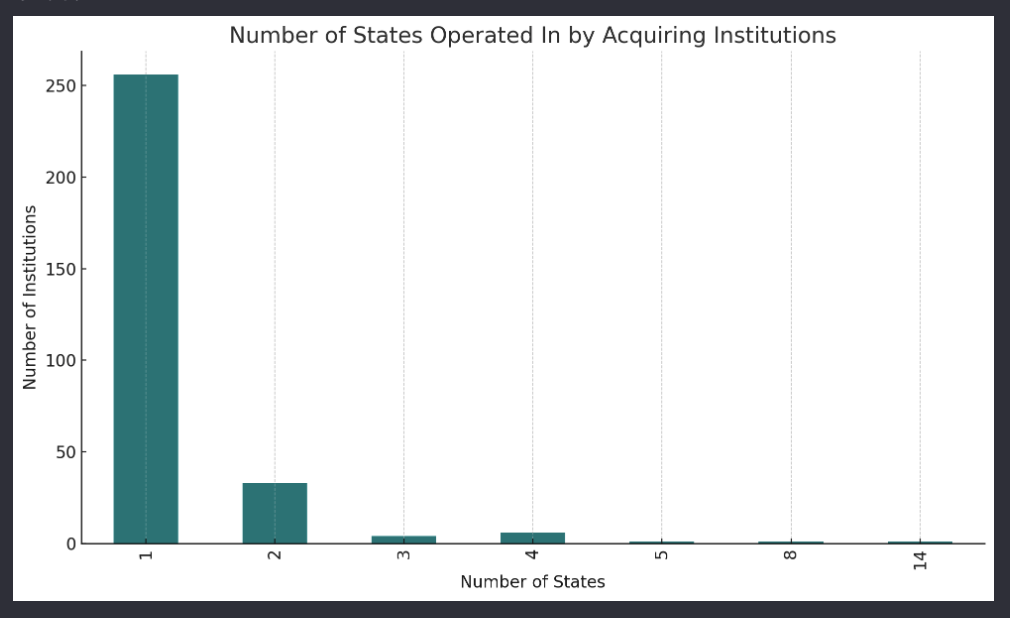

Almost 85% of Failed Banks Were Acquired by Local Institutions

When a bank fails, the FDIC typically arranges an acquisition by another bank to smooth the transition for customers. Analysis of these acquiring institutions provides clues on the size and breadth of the failed banks.

The vast majority of acquirers — 256 out of 302 — operate in just one state. This suggests that most failing banks tend to be smaller regional and community banks rather than large national institutions. Local competitors can more easily absorb these smaller banks.

However, a minority of acquisitions involve banks with multi-state footprints:

- 33 acquirers have operations in 2 states

- 4 operate in 3 states

- 6 have a presence in 4 states

- A handful operate in 5 states or more.

The participation of these broader institutions implies that some fraction of failures do include larger regional or national banks whom they gobble up. Banks with operations spanning five or more states have the resources and infrastructure to integrate much bigger assets.

So while community banks certainly suffer the most losses, the crisis still dragged down some substantial regional banks. The acquisition patterns reflect two tiers of failures — smaller local banks with localized acquirers, as well as larger regional banks being absorbed by national players. Understanding these nuances can help gauge the root causes behind differing bank failure trajectories.

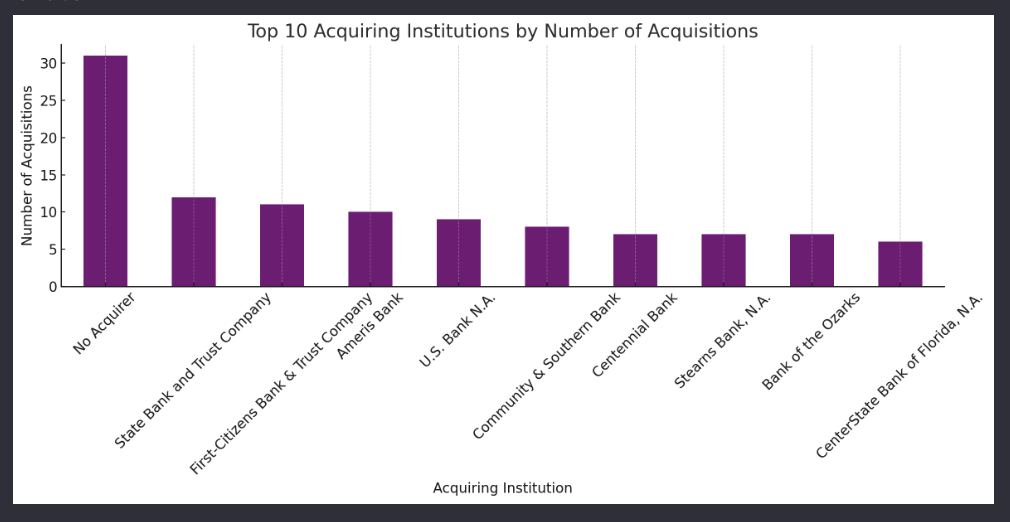

Large Banks Grew Assets by 2-3x Through Failed Bank Acquisition

When banks fail, other institutions step in to acquire them and maintain operations. Analysis of the bank “lifelines” in the FDIC data uncovers intriguing details on key acquirers.

Topping the list is “No Acquirer” with 31 instances, likely indicating the FDIC handled the dissolution. Of actual acquiring banks, State Bank and Trust Company purchased the most – 12 failed banks. First-Citizens Bank & Trust snatched up 11 institutions, while Ameris Bank rescued 10 failing peers.

Other frequent acquirers include giants like U.S. Bank (8 acquisitions) and super-regional players such as Community & Southern Bank (9), Centennial Bank (8), and Stearns Bank (8). Bank of the Ozarks and CenterState Bank also participated in multiple deals.

On average, acquirers took over 1.88 banks each, but the breadth of activity varies widely (standard deviation of 2.34 acquisitions). While most absorbed just one failure, prolific acquirers substantially raise the average.

In fact, the median or midpoint number of takeovers per bank is 1, confirming more single-instance deals. But for acquirers with the resources and risk-appetite, the wave of failures brought prime consolidation opportunities.

As the crisis took its toll, a subset of strong capitalized banks scooped up the remnants, sometimes doubling or tripling their asset size almost overnight through FDIC-assisted acquisitions.

Final Thoughts

While the crisis inflicted immense damage, the analysis shows bank failures normalizing to pre-recession levels as recovery took hold. With risk management deficiencies addressed and regulations tightened, the system regained stability. Regional hotspots like Georgia and Florida now mirror national trends of minimal closures. And consolidation has simmered with fewer targets available. While the crisis presented an epic test, the data indicates banks learned critical lessons about navigating uncertainty. With memories fresh and vigilance high, the system is better braced for potential shocks ahead.

Methodology for Analyzing the “FDIC Failed Bank List”

Below, we offer a thorough overview of the data source for this study as well as the analysis techniques and considerations and limitations of the analysis:

Data Source

The dataset titled “FDIC Failed Bank List” was used for the analysis. This dataset was sourced from data.gov, contains information about banks in the United States that have failed, including details such as bank name, city, state, certification number, acquiring institution, closing date, and FDIC fund number.

Analysis Techniques

- Trends Over Time – For analyzing the trends over time, the ‘Closing Date’ column of the dataset was first converted into a datetime format to facilitate time-based analysis. The data was then grouped by the year of the closing date, and the count of bank failures for each year was calculated. This provided a clear picture of how the frequency of bank failures varied over the years. To visually represent these trends, a bar chart was plotted, showing the number of bank failures for each year. This approach highlighted specific years with unusually high or low numbers of bank failures, suggesting potential correlations with broader economic events or regulatory changes.

- Geographical Analysis – The geographical distribution of bank failures was analyzed by focusing on the ‘State’ column. The number of failures in each state was counted to determine which states had experienced the most bank failures. This analysis was visualized using a bar chart, which clearly depicted the variation in bank failures across different states. This provided insights into potential regional economic vulnerabilities or strengths, and helped to identify any patterns or anomalies in the geographical aspect of bank failures.

- Size and Type of Banks – Due to the lack of explicit data regarding the size and type of the failed banks, a proxy approach was utilized. The acquiring institutions were analyzed based on the number of different states they operate in, assuming this to be an indirect indicator of the size and reach of the failed banks they acquired. The data was categorized based on the number of states each institution operates in, and a bar chart was used to illustrate the distribution. This analysis offered a rough estimation of the size and type of the failed banks, albeit with the limitation of being based on an indirect measure.

- Analysis of Acquiring Institutions – This part of the analysis focused on identifying patterns in the acquisition of failed banks. The frequency of acquisitions by each institution was counted to determine the most active acquirers in the dataset. The institutions with the highest number of acquisitions were then highlighted, and a bar chart was used to visually represent these top acquirers. This analysis shed light on the consolidation trends within the banking sector and provided insights into the strategies of various institutions in acquiring failed banks.

Considerations and Limitations

- Data Limitations – The dataset did not provide direct information on the size and type of each failed bank, which limited the depth of analysis in certain aspects.

- Assumptions – Some analyses relied on assumptions, such as using the reach of acquiring institutions as a proxy for the size and type of failed banks.

- Temporal Coverage – The analysis was limited to the time period covered by the dataset, and the insights are relevant within this context.

Frank Gogol

I’m a firm believer that information is the key to financial freedom. On the Stilt Blog, I write about the complex topics — like finance, immigration, and technology — to help immigrants make the most of their lives in the U.S. Our content and brand have been featured in Forbes, TechCrunch, VentureBeat, and more.